The U.S. regulated online casino market is smaller than sports betting in terms of states (eight, soon to be nine, versus 35+), but it's larger where it counts: margins. iCasino operators keep roughly 25-30 cents of every dollar wagered, compared to the 10 cents or so that sportsbooks retain. That math, combined with the lack of seasonal volatility, makes iGaming the more attractive business for operators and a significant tax revenue engine for the states that have authorized it.

This page tracks operator market share, state-level gross gaming revenue, and tax generation across the regulated U.S. online casino market. The charts and statistics below are presented by Casino Reports in collaboration with independent analyst Alfonso Straffon, a longtime industry observer, former sports trader, and equities analyst at Deutsche Bank. We update here on or about the third Thursday each month.

For a deep dive into the sports betting side, visit our companion page: U.S. Sports Betting Market Stats Database.

If you reference any data from this page, please support our work and cite this page with a link. Spotted an error? Reach out to brett@thirdplanet.us.

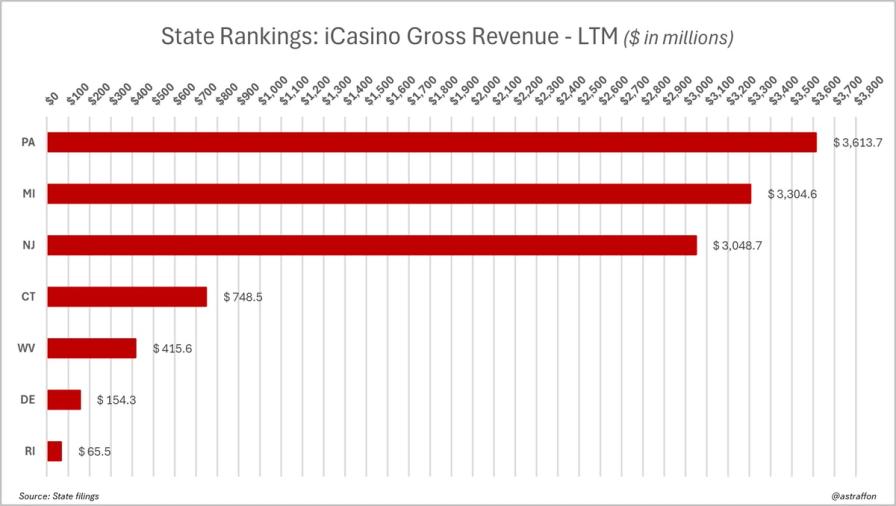

1. iCasino gross gaming revenue by state, LTM (May 2025 through April 2026)

Key Insights:

- Records continue to fall across multiple jurisdictions. Pennsylvania leads the U.S. iCasino market with $3.6 billion in gross gaming revenue over the last 12 months, up from $3.59 billion in the previous LTM frame and $3.42 billion the frame before that. The trajectory has been consistent and upward.

- Michigan and New Jersey closely follow at $3.3 billion and $3.05 billion, respectively. New Jersey has crossed the $3 billion LTM threshold for the second time.

- Connecticut leads the second tier at $748 million, followed by West Virginia at $415.6 million, Delaware at $154 million, and Rhode Island at $65.5 million.

Pennsylvania, Michigan, and New Jersey have cemented themselves as the "revenue triad" in U.S. iGaming, each generating over $3 billion in annual GGR. Major operators and suppliers, including Playtech and Evolution Gaming, have established live dealer studios in all three states.

Maine became the eighth state to legalize iGaming in January 2026 when Gov. Janet Mills allowed LD 1164 to pass into law without her signature. The law grants exclusive online casino rights to Maine's four federally recognized Wabanaki tribes, each of which can partner with one third-party operator. DraftKings and Caesars already have tribal sports betting partnerships in the state, giving them an inside edge. The 18% tax rate is competitive. A launch is expected in late 2026 or early 2027, though a lawsuit from Oxford Casino Hotel (which was excluded from the bill) could delay things.

The bigger question is New York. Sen. Joseph Addabbo Jr. introduced iGaming legislation for the fourth consecutive year in January 2026 (SB 2164), with an Assembly counterpart (A6027) from Assemblywoman Carrie Woerner. The proposed 30.5% tax on GGR is well below the 51% sports betting rate but among the highest contemplated nationally for iCasino.

Two obstacles that had previously blocked progress have been cleared: the downstate casino licensing process wrapped in December 2025 (licenses awarded to Bally's Bronx, Resorts World NYC, and Metropolitan Park), and the state enacted a sweepstakes casino ban. The Hotel and Trades Council remains opposed over job cannibalization concerns, but Addabbo is characterizing 2026 as the clearest path yet. If enacted, New York would instantly become the largest iGaming market in the country by a wide margin, and launch would likely come no earlier than 2027.

In Delaware, the state lottery replaced 888 with Rush Street Interactive at the end of 2023. In September 2024, Rush Street launched live dealer games through Evolution Gaming, available through all three of the state's licensed casinos.

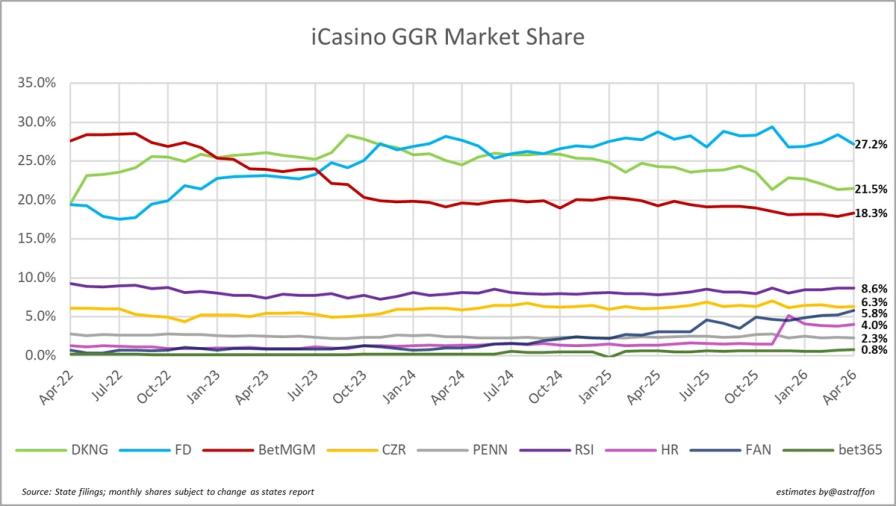

2. iCasino GGR market share by operator (March 2022 to present)

Key Insights:

- FanDuel Casino set a new record share at 29.4% in November 2025, settling back to 27.2% as of April 2026. In February 2025, FanDuel went live with the exclusive Huff N' More Puff, a digital version of the wildly popular on-floor slot, which helped accelerate its share growth. FanDuel has also pushed World of Wonka and other exclusive titles throughout the year.

- DraftKings Casino sits at 21.5%, maintaining steady growth. DraftKings has been innovating with a form of peer-to-peer poker available in certain states through its casino app, while also expanding its content library and Golden Nugget Online Gaming and Jackpocket Casino brands.

- BetMGM's decline across the past four years is the most notable story in this chart. It surged to 28% share during the post-launch phase in Michigan (January 2021) and has since fallen roughly 10 points to 18.3%. That lost share has gone almost entirely to FanDuel and DraftKings.

- Fanatics Casino at 5.8% has nearly tripled its share from a year ago. Hard Rock has climbed to 4.0%, and the Seminoles are also veering into products resembling iGaming in Florida where they hold a state monopoly.

- Rush Street Interactive (BetRivers/PlaySugarHouse) continues to punch above its weight, stable and rising to 8.6% share. Frequently rumored as an acquisition target, RSI has held at roughly 8-9% for years.

Revenues from multiple brands under the same parent company are combined. Flutter includes FanDuel and PokerStars; DraftKings includes Golden Nugget Online Gaming and Jackpocket Casino; BetMGM includes Borgata.

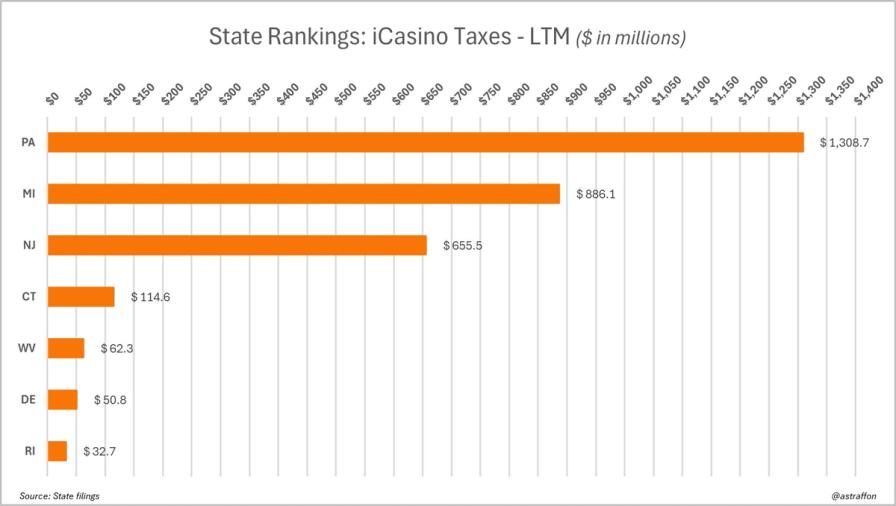

3. iCasino tax revenue by state, LTM (May 2025 through April 2026)

Key Insights:

- Pennsylvania leads with $1.31 billion in iCasino tax revenue over the LTM, driven primarily by its 54% tax rate on online slot machine games. That single rate on slots carries most of the weight; table games and poker are taxed at a far more reasonable 16%.

- Michigan follows at $886.1 million, benefiting from a graduated tax rate that reaches 28% for the largest operators. Michigan regulators have also been aggressive in pursuing enforcement against unregulated and black market operators, intended to protect both citizens and the state's licensed operators.

- New Jersey generated $655.5 million, reflecting the increase from a 17.5% effective rate to 19.75% under Gov. Phil Murphy's FY 2026 budget (effective July 1, 2025). The full-year impact of the higher rate won't be visible until the next LTM cycle.

- Connecticut leads smaller states at $114 million, followed by West Virginia ($62 million), Delaware ($50 million), and Rhode Island ($32.7 million).

This chart, taken together with the GGR figures above, reveals that Michigan and New Jersey remain the most profitable states for operators owing to their more modest tax rates. Pennsylvania's operators gross the most revenue overall, but the 54% slot tax significantly compresses their margins on that product.

| State | iCasino Tax Rate | Notes |

|---|---|---|

Pennsylvania | Variable | 54% on slots, 16% on table games, 16% on poker |

Michigan | Graduated to 28% | Rate rises with revenue; 28% on AGR above $12M |

New Jersey | 19.75% | Increased from 17.5% effective July 2025 |

Connecticut | 18% | Tribal-operated (Mohegan Sun and Foxwoods) |

West Virginia | 15% | Five licensed casinos |

Delaware | ~30%+ | State lottery-operated; revenue sharing model |

Rhode Island | ~50%+ | State lottery-managed; high effective rate |

Maine (signed Jan. 2026) | 18% | Tribal-exclusive; launch expected late 2026/early 2027 |

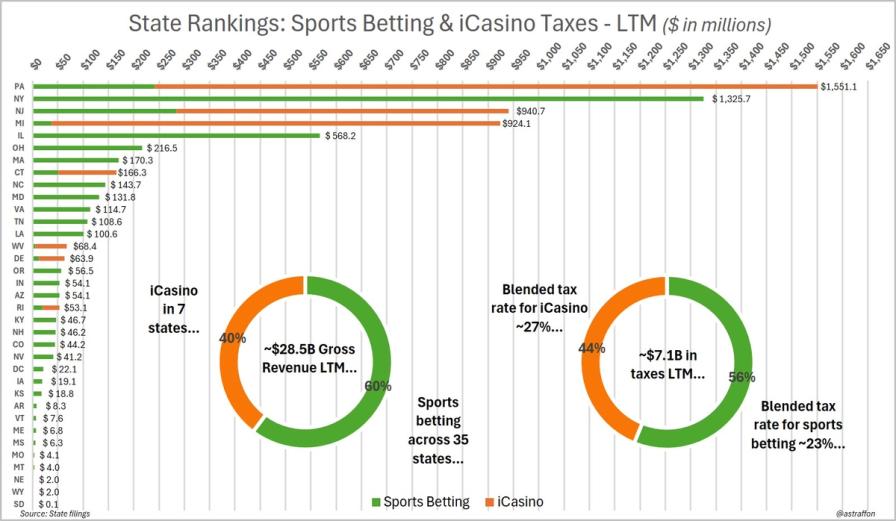

4. Sports betting and iCasino taxes combined, LTM (May 2025 through April 2026)

Key Insights:

- With just seven states having legalized regulated online casinos (Maine's law is signed but not yet live), those states account for 40% of all gross gaming revenue when combining sports betting and iGaming figures, and 44% of tax dollars collected, reflecting slightly higher effective tax rates on iCasino revenue.

- That is not a typo: New York has nearly matched Pennsylvania ($1.33 billion vs. $1.54 billion) with sports betting tax revenue alone. Pennsylvania's combined total comes from both iCasino and sports betting. If New York legalizes iGaming at the proposed 30.5% rate, this chart will need a longer x-axis.

- The juxtaposition of the two revenue streams underscores a basic market reality: margins are higher and more stable for online casinos than for sports betting, even in the era of rising structured hold and heavy parlay activity. Sports betting has more states, more handle, and more public attention, but iCasino is the better business.

New York levies a 51% tax on gross sports betting revenue on its nine active operators: DraftKings, FanDuel, Caesars, BetMGM, Fanatics, theScore Bet (formerly ESPN Bet), Resorts World Bet, Bally Bet, and BetRivers. Monthly betting volume hovers between $1.5 and $2 billion, translating to the tax haul you see on this chart.

For the full sports betting breakdown, including operator handle and GGR market share, state-level rankings, parlay data, and quarterly hold trends, visit our U.S. Sports Betting Market Stats Database.

Selected data sources

- Michigan Gaming Control Board

- New Jersey Division of Gaming Enforcement

- Pennsylvania Gaming Control Board

Source: State filings. Charts and estimates by @astraffon. Monthly shares subject to revision as states report.