U.S. Sports Betting Data: Market Share Stats By Brand, Gross Gaming Revenue, Parlay Handle, Hold

Here are regularly updated U.S. sports betting market charts, insights, and trends

9 min

If you’re seeking data and statistics to tell the story of the regulated U.S. sports betting market, you have come to the right place and right page.

Our team of journalists and analysts has been studying the regulated market since its inception. With this live database here, built upon state agency filings, we will identify which operators are generating what revenues, state taxes generated in each jurisdiction, how parlay wagering has come to dominate the market, and more.

The charts and statistics below are presented by Casino Reports in collaboration with independent analyst Alfonso Straffon, a longtime industry observer, former sports trader, and equities analyst at Deutsche Bank. The charts will be updated on a monthly basis, on or about the third Thursday, to reflect the latest state filing data.

Also check out the InGame Intel application at our sister site, InGame.com, where you can query the database for information on U.S. sports betting handle, revenue, taxation and other data, and easily generate charts for your own usage.

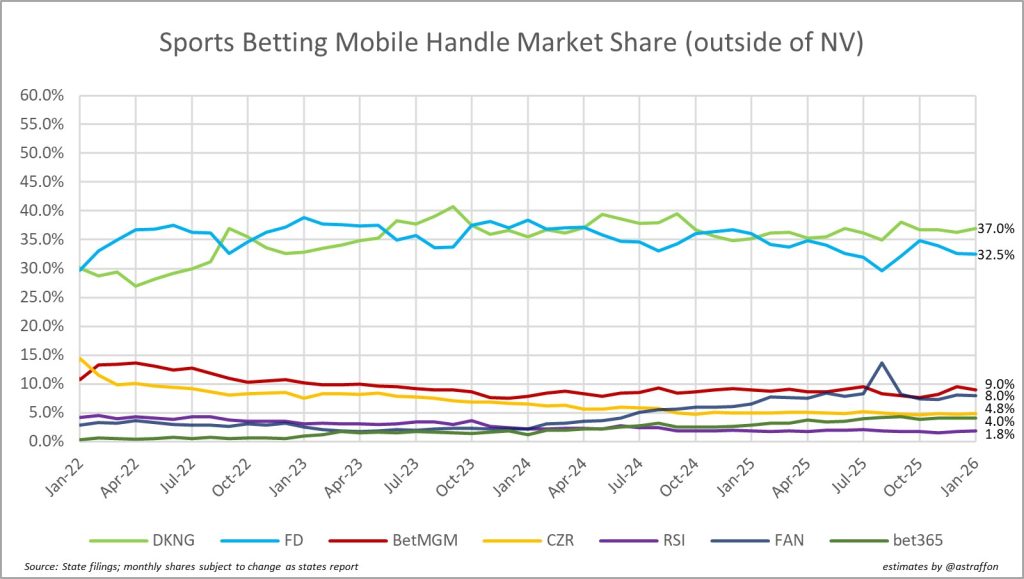

1. Sports betting handle market share (January 2021 to present)

Key Insights:

- DraftKings Sportsbook reclaimed the handle crown from FanDuel once again in May 2025 and has held it since, current to February 2026. The advantage has remained fairly static in recent months with DraftKings currently leading by 4.5 percentage points.

- The August 2025 surge by Fanatics, which jumped all the way up to 14.3% apparently at the expense of the duopoly, probably was inflated by promotional spending in the run-up to football season, or if not that, by VIP activity. As of Nov. 2025, Fanatics returned to a previous level at 7.7%.

- Dating to at least January 2021, the duopoly of FanDuel Sportsbook and DraftKings Sportsbook has hovered between approximately 30 and 40% each for market share of the nationwide regulated sports betting handle — i.e., dollars wagered/risked by bettors (irrespective of wins and losses).

- That combined market share currently totals 72.3% of the dollars wagered in the regulated U.S. market, down slightly from historical highs of around 75%.

- BetMGM, Fanatics, and Caesars comprise the (distant) second tier. They have oscillated between about 2% and 11% apiece for the national market share.

- ESPN Bet at 2.6% proved an obvious, glaring disappointment, and to nobody’s surprise, PENN Entertainment, which had been leasing ESPN’s brand for the sportsbook, exercised an opt-out clause on Nov. 6, which will shutter the brand, with PENN transitioning to theScore Bet, which it had previously acquired.

Notes: The yellow spike in January 2022 for Caesars reflects an auspicious advertisement-and bonus-fueled start in New York state, coinciding with the NFL playoffs. Unfortunately for Caesars, the momentum did not last. However, Caesars’ share has held steady in the 6-7% range for both sports betting and the more lucrative iCasino sector.

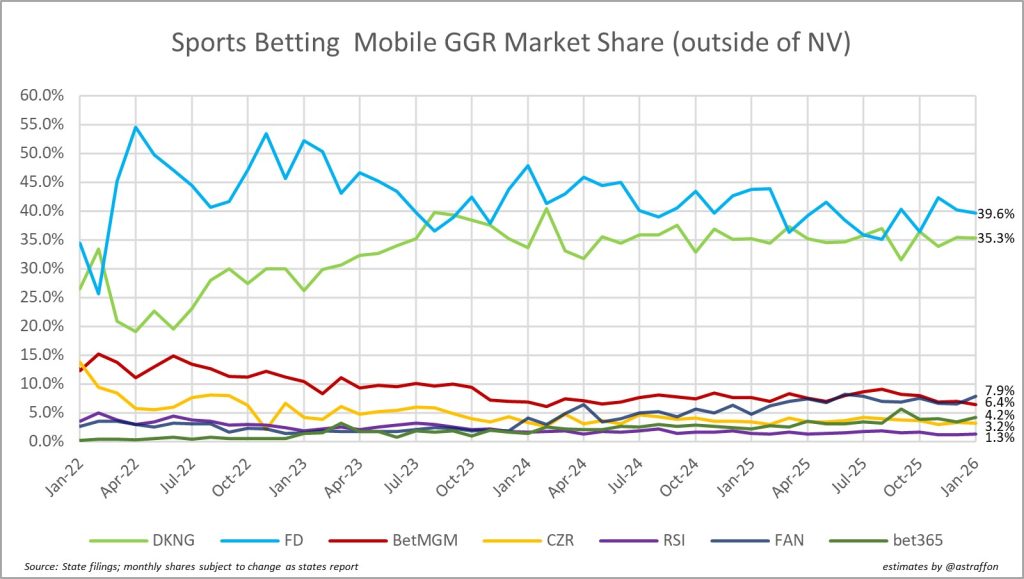

2. Sports betting market share by gross gaming revenue (GGR) (January 2021 to present)

Key Insights:

- With filings available through February 2026, including the full NFL season, FanDuel and rival DraftKings have zigged and zagged through with FanDuel surging ahead to current mark of 39.6 to DraftKings’ 35.3%.

- In general, FanDuel has historically had higher mixture of parlay bets (this disparity may have evaporated) and correspondingly greater hold percentage, although that also makes it subject to some volatility when the chalk (favorites) align.

- FanDuel’s parent company Flutter believes that it possesses superior abilities and systems for pricing and risk-management and an overall more effective parlay engine.

- Fanatics has been approaching 10% of the sports betting GGR pie with 8.3% in June 2025, but slipped a bit to 6.9% as of present as it guns for a podium position that is a not-so-distant third.

Notes: Hard Rock Bet, a well-financed Seminole Tribe-backed product, will leverage its monopoly position in Florida for gains across the country. Figures from Florida do not get reported and therefore are unknown publicly.

Also note that the impact of prediction markets — leaders Kalshi and Polymarket — but also DraftKings and FanDuel’s own vehicles — are not visible in these percentage figures. A March 24 note from Citizens analyst Jordan Bender sheds some light on the overall impact: “Overall, management commentary during 4Q25 earnings calls suggested limited impact from the prediction markets, with estimates of 0% to 5% cannibalization of the sports betting market, in the range of our view of 5%,” Bender writes. “That said, it still raises questions about the source of sports trading volume on the prediction market sites.”

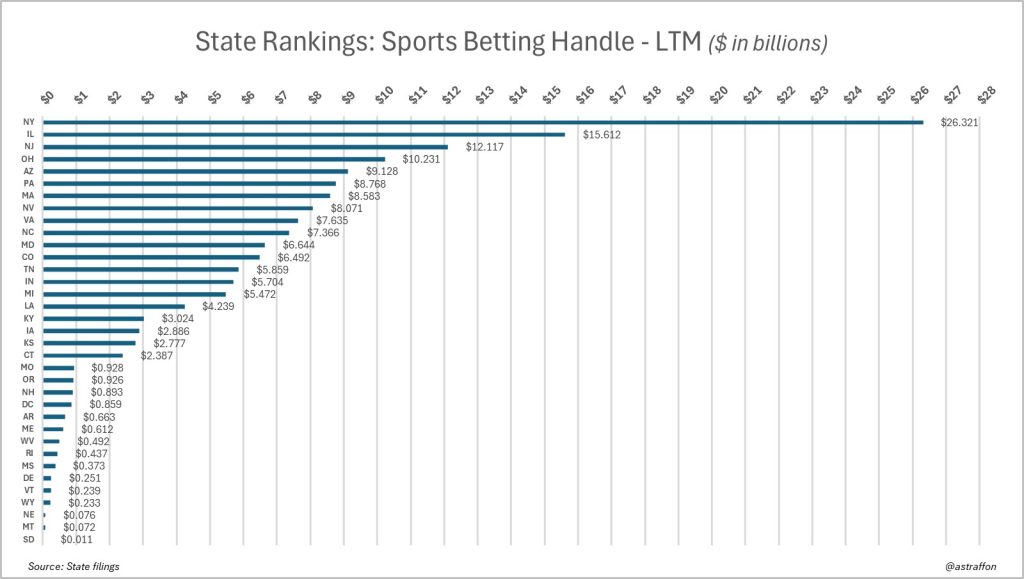

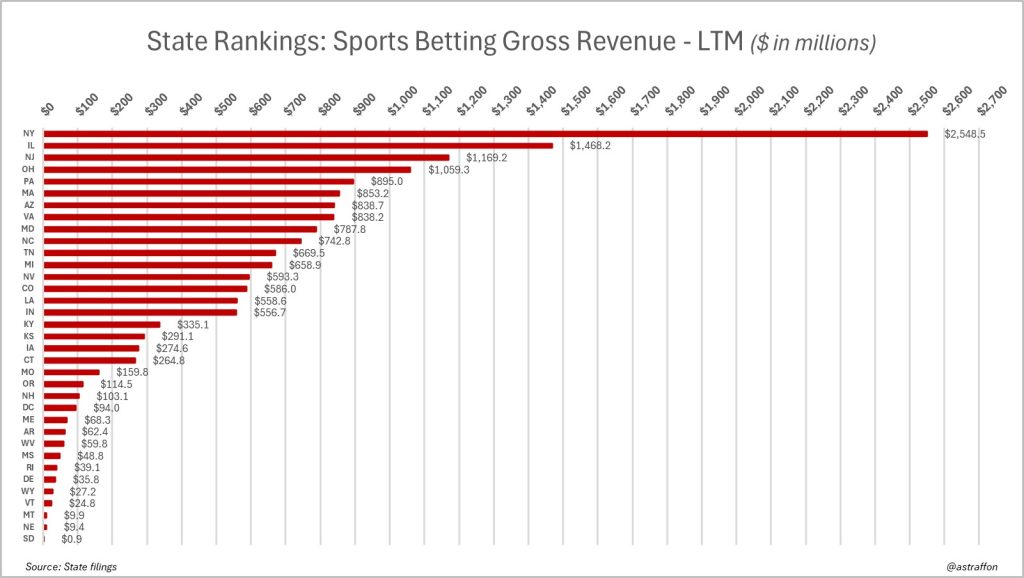

3. Sports betting handle by state, last twelve months (LTM) (2026)

Key Insights:

- That’s a whopping $26.3 billion wagered at New York over the last 12 months. New York’s nine regulated sportsbooks have handled more on average per month (about $2.16 billion) than more than a dozen of the other states’ totals LTM.

- That’s not terribly surprising given the population of New York and its relatively high per capita income, buoyed by zip codes around New York City, Long Island, and Westchester County.

- Oregon and New Hampshire, where DraftKings owns a sportsbook monopoly, have challenged for $1 billion handle for a calendar year, but both fell a bit short at $927 million and $866 million, respectively.

Notes: Mississippi regulators and lawmakers have repeatedly flirted with authorizing online sports betting — most recently in Jan. 2026 — but for now it remains a state with on-premises betting at casinos only.

If or when Texas and California join the ranks of the regulated U.S. sports betting states — something that Las Vegas Sands is determined to make happen, at least in Texas, based on spending — it will be interesting to see how the top of the chart shakes out.

4. Sports betting gross revenue by state, LTM through (2026)

Key Insights:

- Operators are generating large sums in New York — a collective 2.55 billion grossed over the last 12 months — but also had to pay a $25 million up-front licensing fee for the privilege of doing business in the state. New York also levies a nation-leading 51% tax on the GGR generated by its authorized sportsbooks (tied with Rhode Island, Illinois and Vermont for the highest).

- Do not conflate gross revenue with net revenue or with net profit (money left over after all expenses—including taxes, interest and operating costs).

- North Carolina is a relative sports betting newcomer, having launched its online market in January 2024 to industry and consumer fanfare. It’s early but, after two year,s the state’s GGR has climbed past Michigan and into the top 10.

- Illinois had been one of the more lucrative states for operators. In June 2024, however, Gov. JB Pritzker signed into law a state budget that instituted a new progressive tax scheme effective July 1, 2024.

Notes: The law raises the privilege tax on a licensee’s annual adjusted gross sports wagering receipts (AGSWR) to the following rates:

- 20% of annual AGSWR up to and including $30 million;

- 25% of annual AGSWR in excess of $30 million but not to exceed $50 million;

- 30% of annual AGSWR in excess of $50 million but not to exceed $100 million;

- 35% of annual AGSWR in excess of $100 million but not to exceed $200 million;

- 40% of annual AGSWR in excess of $200 million.

The 40% tax will be felt only by DraftKings and FanDuel, which was the intent of the tax structure modification. The other market participants, barring a surge in revenue, will not reach the thresholds subjecting them to the higher rates.

The taxation situation has become even more precarious and onerous in top the two operators in Illinois. In June 2025, the legislature passed a budget bill that contained an additional per-wager tax — 25 cents for an operator’s first 20 million wagers, 50 cents for wagers above that.

On June 10, FanDuel announced in response that it would impose a 50-cent transaction fee on all wagers placed in Illinois, effective Sept. 1. The company said that if Illinois lawmakers were to eliminate the new tax, it would do the same with its own new line item. Most other Illinois sportsbooks followed with a per-bet fee or the imposition of minimum bet amounts ($1 or $2) to head off losses.

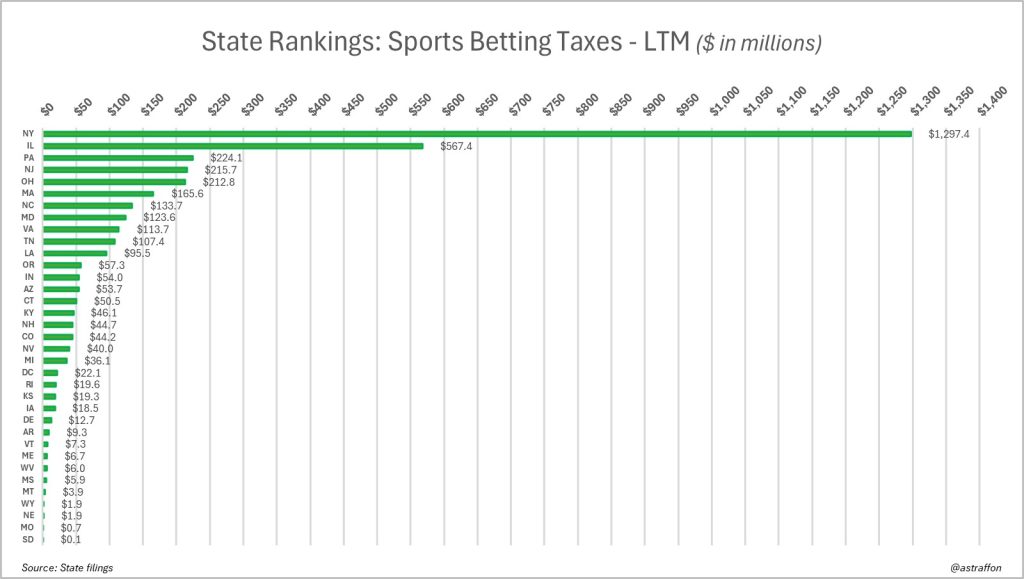

5. Sports betting taxes generated by state, LTM through (2026)

Key Insights:

- The tax structure modifications in Illinois has resulted in the state jumping into second place in recent months. Over the last 12 months, it checks in at $567.4 million and will close the gap further throughout 2026.

- New York has collected by far the most tax revenue from sports betting with its 51% tax rate on GGR, good for $1.297 billion for 12 months spanning February 2025 through February 2026.

- Effective June 2023, Ohio raised its tax rate on operator GGR from 10% as established at the time of legalization to 20% — and contemplated raising it again. Consider that Ohio’s haul would be roughly halved and would slide in alongside Maryland if not for the adjustment.

- Pennsylvania also sits on the higher end of the scale with its 36% rate on operator GGR, which was established at the time of sports betting legalization in the state. The state has generated $194.2 million over the LTM, fourth only to New York, Illinois, and Ohio. The results of the Super Bowl, in which the Philadelphia Eagles annihilated the Kansas City Chiefs, was not a fiscally favorable results for the house.

Notes: Illinois’ shift from 15% to a progressive structure and further per-bet increase had ripple effects in other states, with lawmakers developing an appetite to turn up the dial on operators. These tax increases on the base rates have been realized in other states:

- New Jersey Gov. Phil Murphy proposed increasing the sports betting tax rate from 13% to 25% (and iGaming tax rate from 15% to 25%) in his 2025 budget. Ultimately the governor and lawmakers settled on a new rate for both sports betting and iGaming at 19.75%.

- Maryland’s rate increased from 15% to 20% via Gov. Wes Moore’s Budget Reconciliation and Financing Act of 2025, less than the doubling Moore had sought.

- Louisiana‘s Senate in June approved a tax increase on digital sports betting revenue from 15% to 21.5%. That change is over to Gov. Jeff Landry for signature.

- North Carolina might grow from 18% to 36% if the House budget reflects the Senate’s desire to double up on operators. This one is pending as of Sept. 2025.

- Multiple additional jurisdictions, including Indiana and Ohio, are considering similar proposals.

- Pennsylvania in Nov. 2025 considered changes as well and on taxing skill games, but ultimately backed off.

This is a 2024 update for background and posterity: The 2024 Illinois increase triggered a response from the operator side. DraftKings, coinciding with its third-quarter earnings report, floated a plan in August last year to pass the elevated Illinois tax back to the bettor as a surcharge on winning bets. To say the idea was roundly rejected and panned would be putting it mildly. But it took until FanDuel (Flutter) during its own earnings call two weeks later said it absolutely would not follow DraftKings’ lead and for DK to publicly abandon the idea and try to save face. Still, DraftKings CEO Jason Robins has said the company will consider any and all ideas to protect its margins. Back to the drawing board in Illinois.

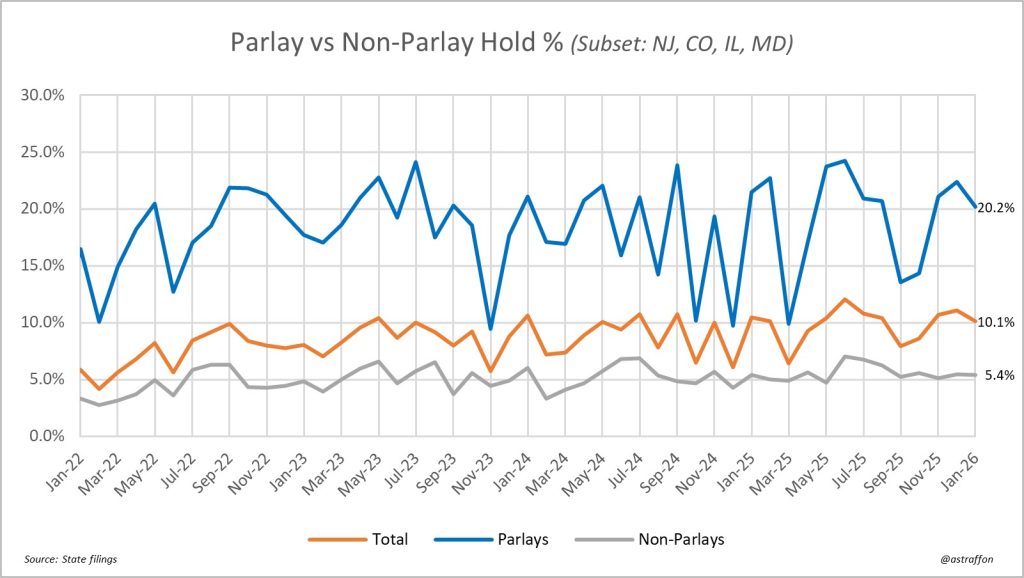

6. Parlay hold % versus non-parlay hold (January 2021 to present)

Key Insights:

- What goes down must go up. There’s a good amount of volatility from month to month, but the overall, long-term trend for hold percentage at U.S. regulated sportsbooks is upward. This is due to a variety of factors, including customer adoption and familiarity with Same Game Parlay (SGP) wagers, improvements in operator pricing, and operator emphasis on serving up these higher-margin offerings in its favor.

- This chart contemplates the betting activity in New Jersey, Colorado, Illinois, and Maryland only, though it’s a pretty nice sample considering the overall volume in these states. The data reporting into granular bet kinds like parlays is more robust and transparent in some states than in others.

- The highest parlay hold percentage we have observed is approximately 26% in November 2021 and then again in June 2025 (25.8%), which then sharply turned in the other direction in the ensuing months.

- For the most part, the hold percentage on parlay bets and non-parlay bets is correlated — i.e., when one goes up or down, usually the other does, too.

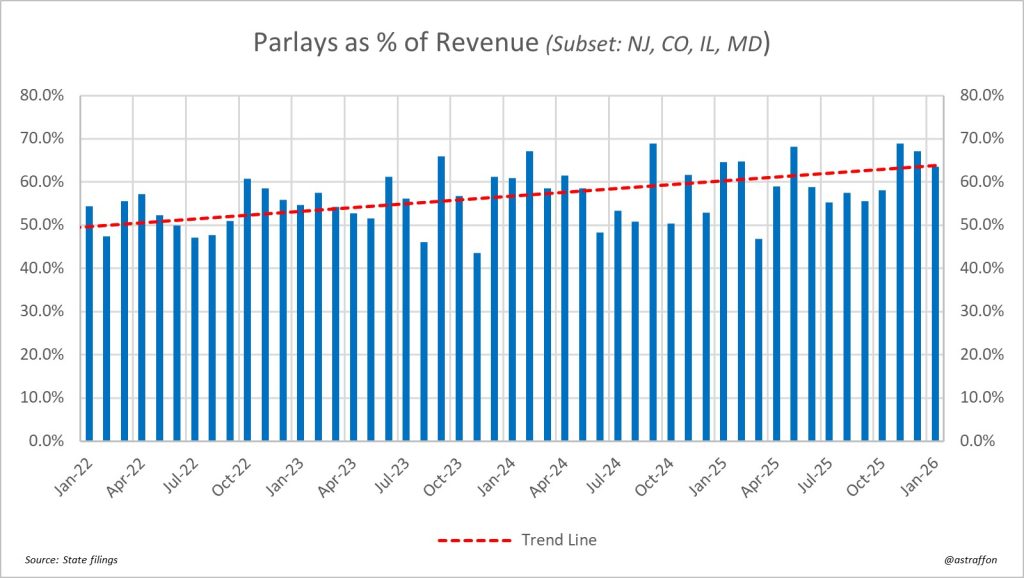

7. Parlay betting revenue’s percentage of overall betting revenue (January 2021 to present)

Key Insights

- This line spiked near an all-time high at 69% in November 2025 after a dip earlier in the football season. Back at the 60% mark as of February 2026.

- The bettors had their way thanks to a favorites-heavy NCAA men’s basketball tournament in March 2025, collectively knocking the parlay revenue to below half of operator revenue (47%), which had only happened in three other months since the start of 2023. It has settled back into the mid-50s.

- Prior to that, the percentage of revenue derived from parlay bets climbed to 69% in September 2024 as the trendline remains angled upwards.

- While the sample is indeed a subset of the regulated market nationally, the four states supplying this data are qualitatively a broad and diverse sample.

- How high can the figures go here? We shall see as it’s probably limited only by ingenuity, tempered in some places by desire to not burn out bankrolls.

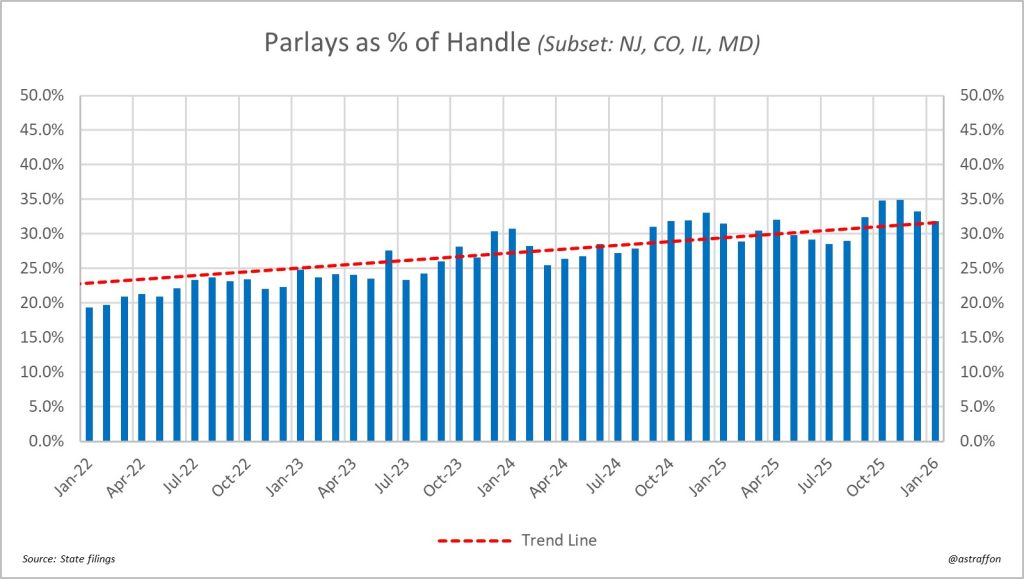

8. Parlay betting as a percentage of overall handle (January 2021 to present)

Key Insights:

- We saw a new record here in January 2026: the percentage of parlays of overall handle reached 35.1%, before settling back down to 31% in February 2026.

- Dating back almost four years, this number has grown from around 20% of overall handle to 33% for December 2024 and a year later to a new peak.

- The ceiling here isn’t limitless, as long as there are VIPs in the regulated market making large straight wagers on football and basketball.

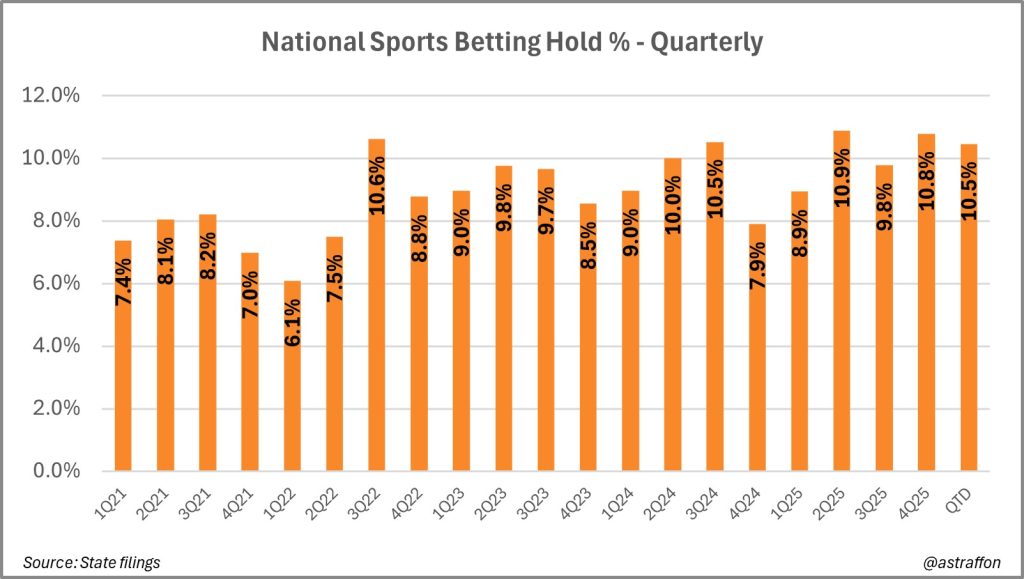

9. National sports betting hold percentage on quarterly basis (January 2021 to present)

Key insights:

- 1Q26 is tracking consistently in the mid-10s within the range established in 3Q22.

- 2Q25 with a 10.9% national hold represents an all-time high in our charting.

- 3Q25 had been trending slightly above but concluded now on Sept. 30, the figure settled back down to 10%.

- In October and December 2024, the Q4 figure dropped to 7.9% on the back of “customer-friendly” NFL results — i.e., lots of favorites covering. Booking sports can be a volatile business, even in the era of parlays.

- The quarterly handle has reached or exceeded 10% five times now: 3Q22 at 10.6%, 2Q24 at 10%, and 3Q24 at 10.5%, 2Q25 at 10.8%, and 10.4% in 4Q25.

- If you’re going to bet on which way this number is going, it probably would be wise to play the over on 10% for future quarters.

- Historically, pre-PASPA when Nevada was the main vein for regulated betting in the U.S. and parlays were given far less emphasis, this number lived closer to 5% than 10%.

Please go here to visit our other database: US Online Casino Data — Market Share By Brand, Gross Gaming Revenue Stats, And Taxation

Selected data sources: